from Web Hosting Talk:

>>Do NOT trust Internap

On the night of April 28th the 365Main facility in Chandler, AZ lost power to 2 data floors. That is about 20,000-30,000 sq feet of colo space that went down. The downtime lasted for over 10 minutes. I should mention that my contract with Internap specifically says a 100% power uptime SLA. Not 4 9's, not 5 9's, 100%. It was later determined to be human error that caused the facility to go dark, but that's not my problem.

...

The moral of this story is that every single person at Internap that I have mentioned is unhelpful, unresponsive, and leaves much to be desired in terms of customer satisfaction.

The impression that I get from these Directors and VP's is that of arrogance. They can't be bothered to return voicemails from unhappy customers, or answer emails providing status updates. How dare a lowly customer speak to them when they have peons below them to handle us worthless customers.

Hopefully my story will drive as many sales away from Internap as possible. I can only hope that no one else has to deal with the customer dis-service that is Internap.

-----

With one contract exception, I've generally had a good experience with Internap. But I agree that their customer service overall has declined somewhat in the last year or two, probably because of the cost cutting they've had to do to turn the company around. And I don't typically work with on things like billing disputes, and that's generally the weakest link in many companies; perhaps my perception would be worse if I had to deal with those issues like you.

...

And while I wish you luck (and you'll probably need it, as Internap is not some small mom-and-pop shop that lets people out of contracts willy-nilly), I'm not aware of any company that's going to let you out of a contract for 10 minutes of downtime.

-----

We were with Internap from 2002-2009.

Internap offers a great product with exceptional stability and engineering support, but their billing/account support functions are not very efficient (that's putting it nicely). We've had billing/contract/order issues that took a year to resolve. Yes, they can be THAT slow. You have to understand going in that their business model is built around providing service to large enterprises, and unless you're spending a minimum of $10K/month, you're really not that important to them. Maybe the number is $100K/month, who knows. I suspect we were one of their smallest colo accounts (period), so my service expectations were set accordingly. But anyway, for better or worse that's the bottom line as to why you don't get much love when you contact them.

...

Saturday, May 15, 2010

Amended Facility

On May 10, 2010, Equinix Australia Pty Ltd., Equinix Hong Kong Limited, Equinix Singapore Pte. Ltd., Equinix Pacific Pte. Ltd and Equinix Japan K.K. (all indirect, wholly owned subsidiaries of Equinix, Inc. (“Equinix”) and, collectively, the “Borrowing Group”) amended a multi-currency credit facility agreement for approximately $170,000,000 in local currency equivalents (the “Facility”) with DBS Bank Ltd., ING Bank, N.V., Singapore Branch, The Royal Bank of Scotland N.V. and GE Commercial Finance (Hong Kong) Ltd., as Joint Mandated Lead Arrangers and as Joint Mandated Bookrunners (the “JMLAs”) and The Royal Bank of Scotland N.V., as Facility Agent (the “Amended Facility”). The Amended Facility has been increased to approximately $200,000,000 in local currency equivalents and adds HSBC, OCBC, Commerzbank, Citibank and Indian Bank as lenders.

The Amended Facility has a five-year term, and consists of two tranches. The first tranche is available for immediate drawing upon satisfaction of certain conditions precedent under the Amended Facility and will be used to refinance existing secured loans within the Borrowing Group. The second tranche provides for a delayed draw option of up to 24 months following the signing date of the Amended Facility. The Amended Facility carries an initial borrowing margin of 3.50% over the local borrowing rates for the first 12 months and provides for a reduction to a margin of 2.50% over the local borrowing rates depending on the leverage ratio within the Borrowing Group. The Amended Facility contains financial covenants with which the Borrowing Group must comply, which consist of leverage ratios, an interest expense coverage ratio and a debt service coverage ratio. The Amended Facility is guaranteed by Equinix and secured by certain of the Borrowing Group’s assets and share pledges.

Initial drawings under the Amended Facility occurred on May 14, 2010. The first tranche in the amount of approximately $81,000,000 in local currency equivalents has been drawn to repay existing term loan facilities. In addition, approximately $16,154,972 in local currency equivalents of the second tranche was drawn to fund capital expansion requirements in Singapore. The remainder will be drawn down over a 24-month period from May 10, 2010.

DBS Bank Ltd. and The Royal Bank of Scotland N.V. are currently lenders to entities within the Borrowing Group under existing credit facility agreements that will be repaid in connection with entering into the Amended Facility.

| Item 1.02. | Termination of a Material Definitive Agreement |

On May 14, 2010, members of the Borrowing Group prepaid and terminated an approximately $88,000,000 multi-currency credit facility agreement, originally with ABN AMRO Bank N.V as lender, facility agent, arranger and collateral agent, as evidenced by a Facility Agreement and related Equinix guarantee, each dated August 31, 2007, as amended (the “Terminated Facility”). The Terminated Facility was used to fund capital expenditures on leasehold improvements, equipment, and other installation costs related to expansion plans in the Asia-Pacific region. Approximately $56,800,000 in local currency equivalents was outstanding under the Terminated Facility on the date of repayment.

The Royal Bank of Scotland N.V., the lender under the Terminated Facility, is also a lender under the Amended Facility described above.

Friday, May 14, 2010

Prostate cancer study results from Netherlands

HT to yyy60 on the IV MB:

UROTODAY

CyberKnife stereotactic radiotherapy as monotherapy for low- to intermediate-stage prostate cancer: Early experience, feasibility, and tolerance - Abstract

Friday, 14 May 2010

Department of Radiation Oncology, Daniel den Hoed Cancer Center, Rotterdam, The Netherlands.

The CyberKnife (CK), a linear accelerator mounted on a robotic device, enables excellent dose conformation to the target and minimizes dose to surrounding normal tissue. It is a very suitable device for performing hypofractionated stereotactic body radiotherapy as monotherapy for low- to intermediate-risk prostate cancer patients. We report our early experience using this technique.

Between June 2008 and June 2009, 10 patients underwent CK monotherapy as treatment for their prostate cancer (stage < /=T2b, Gleason score (GS) < /=7, initial PSA < /=15 mug/L). The prescribed dose was 38 Gy in four daily fractions of 9.5 Gy. The International Prostate Symptom Score and Radiation Therapy Oncology Group symptom scale were prospectively administered before and at 0.5, 1, 2, 3, 6, and 12 months.

Median age of the patients was 71 years (range, 66-76). Three patients had stage T2a and 7a T1c disease, one patient had GS of 7, and all others had GS of 6. Median follow-up was 5.1 months. Median initial PSA was 8.3 ng/mL (range, 1.3-13.6 ng/mL). Median planning target volume delineated on computed tomography after matching with the magnetic resonance imaging scan was 107 cc (range, 42-158 cc). The median V100 of the prostate was 95.8% (range, 94.8-97.2). The D95 of the prostate was 38.3 Gy (range, 38.1-38.8 Gy). The constraints for the bladder, rectum, and urethra were well met. The International Prostate Symptom Scores after 3 months were stable compared with the pretreatment scores. Urinary and bowel Radiation Therapy Oncology Group symptoms were mild and within the expected levels.

This regimen of stereotactic CK monotherapy for low- to intermediate-risk prostate cancer with excellent dose coverage of the prostate was well tolerated. Data collection is ongoing for further assessment of toxicity and PSA response.

Written by:

Aluwini S, van Rooij P, Hoogeman M, Bangma C, Kirkels WJ, Incrocci L, Kolkman-Deurloo IK. Are you the author?

Reference: J Endourol. 2010 Apr 30. Epub ahead of print.

PubMed Abstract

PMID: 20433370

UROTODAY

CyberKnife stereotactic radiotherapy as monotherapy for low- to intermediate-stage prostate cancer: Early experience, feasibility, and tolerance - Abstract

Friday, 14 May 2010

Department of Radiation Oncology, Daniel den Hoed Cancer Center, Rotterdam, The Netherlands.

The CyberKnife (CK), a linear accelerator mounted on a robotic device, enables excellent dose conformation to the target and minimizes dose to surrounding normal tissue. It is a very suitable device for performing hypofractionated stereotactic body radiotherapy as monotherapy for low- to intermediate-risk prostate cancer patients. We report our early experience using this technique.

Between June 2008 and June 2009, 10 patients underwent CK monotherapy as treatment for their prostate cancer (stage < /=T2b, Gleason score (GS) < /=7, initial PSA < /=15 mug/L). The prescribed dose was 38 Gy in four daily fractions of 9.5 Gy. The International Prostate Symptom Score and Radiation Therapy Oncology Group symptom scale were prospectively administered before and at 0.5, 1, 2, 3, 6, and 12 months.

Median age of the patients was 71 years (range, 66-76). Three patients had stage T2a and 7a T1c disease, one patient had GS of 7, and all others had GS of 6. Median follow-up was 5.1 months. Median initial PSA was 8.3 ng/mL (range, 1.3-13.6 ng/mL). Median planning target volume delineated on computed tomography after matching with the magnetic resonance imaging scan was 107 cc (range, 42-158 cc). The median V100 of the prostate was 95.8% (range, 94.8-97.2). The D95 of the prostate was 38.3 Gy (range, 38.1-38.8 Gy). The constraints for the bladder, rectum, and urethra were well met. The International Prostate Symptom Scores after 3 months were stable compared with the pretreatment scores. Urinary and bowel Radiation Therapy Oncology Group symptoms were mild and within the expected levels.

This regimen of stereotactic CK monotherapy for low- to intermediate-risk prostate cancer with excellent dose coverage of the prostate was well tolerated. Data collection is ongoing for further assessment of toxicity and PSA response.

Written by:

Aluwini S, van Rooij P, Hoogeman M, Bangma C, Kirkels WJ, Incrocci L, Kolkman-Deurloo IK. Are you the author?

Reference: J Endourol. 2010 Apr 30. Epub ahead of print.

PubMed Abstract

PMID: 20433370

Managing and Reducing Latency

Equinix is co-sponsoring a thought leadership series - a free series of recorded round table panels focused on technology, trends, and regulations impacting high frequency trading. Stewart Orrell, senior manager of Financial Services, is representing Equinix.

Module 1 is a discussion about "Managing and Reducing Latency." Topics include "Managing the End-to-End Latency Budget" and "New Technologies to Help Reduce Latency."

landing.equinix.com

Thursday, May 13, 2010

Ramius Delivers Letter to CEO and Board of Directors of Immersion Corporation

Intends to Withhold Votes for Election of Directors at Company's 2010 Annual Meeting

Reiterates Need for Direct Shareholder Representation on the Board of Immersion

Expresses Concern With Company's Decision to Nominate David Sugishita

NEW YORK, May 13 /PRNewswire/ -- RCG Starboard Advisors, LLC, a subsidiary of Ramius LLC (collectively, "Ramius"), today announced that it delivered a letter to Victor A. Viegas, Chief Executive Officer, Emily Liggett, Chair of the Corporate Governance and Nominating Committee, and the other members of the Board of Directors of Immersion Corporation ("Immersion" or the "Company") (Nasdaq: IMMR) reiterating its concern that the Board lacks both a vested interest in the financial performance of the Company and expertise in technology licensing and IP litigation. Ramius also expressed disappointment with the Board's decision to nominate Mr. David Sugishita for election at the 2010 Annual Meeting. Ramius beneficially owns approximately 14.6% of the common stock of Immersion.

In the letter, Ramius also questioned the Board's unwillingness to add a seventh director who possesses the attributes Ramius believes are critical to the Company's future success. Ramius also stated that it intends to withhold its votes at the upcoming 2010 Annual Meeting for the election of Mr. Sugishita, but remains open-minded about discussing solutions with the Board to address its serious concerns about Board composition.

The full text of the letter follows:

May 13, 2010 | |

Ms. Emily Liggett (Chair, Corporate Governance and Nominating Committee) | |

Mr. Victor Viegas (Chief Executive Officer) | |

Immersion Corporation | |

801 Fox Lane | |

San Jose, California 95131 | |

CC: Immersion Corporation Board of Directors | |

Dear Emily and Vic: | |

Over the past eight months, we have repeatedly attempted to engage in meaningful discussions with you and other members of the Board of Directors (the "Board") regarding Board composition at Immersion Corporation ("IMMR" or the "Company"). RCG Starboard Advisors, LLC, a subsidiary of Ramius LLC, and certain of its affiliates (collectively, "Ramius"), is the largest shareholder of Immersion owning approximately 14.6% of the shares outstanding. Our interests are directly aligned with the interests of all shareholders in seeking to improve the quality and effectiveness of the Board. From the outset, we have been very clear that the Board lacks both a vested interest in the financial performance of Immersion and expertise in technology licensing and IP litigation. None of the existing directors of Immersion has a substantial financial stake in the Company nor has any director purchased shares of Immersion on the open market in the recent past. As of the 2010 proxy statement filed on April 29, 2010, the directors combined owned a total of just 82,084 shares outright (excluding granted stock options) This represents a mere 0.3% of the outstanding shares. Further, none of the independent directors has direct experience in technology licensing and IP litigation, a key component of Immersion's business strategy.

These two criteria are absolutely critical attributes for the Board. Yet the recent announcement that David Sugishita will replace Robert Van Naarden as a nominee for election at the 2010 Annual Meeting neither addresses the lack of technology licensing and IP litigation experience nor provides for a shareholder representative on the Board..

We have other serious concerns about the Board's decision to nominate Mr. David Sugishita for election at the 2010 Annual Meeting. While the Company claims to have conducted an independent process to identify a new, independent Board member, Mr. Sugishita clearly has direct ties to current Chairman Jack Saltich. Both Mr. Saltich and Mr. Sugishita serve on the Board of Atmel Corporation, where Mr. Sugishita serves as Chairman. Further, Mr. Saltich and Mr. Sugishita would constitute one-third of the Immersion Board. Although Atmel is a customer and partner of Immersion, Atmel also competes directly with Cypress Semiconductor, Renesas Electronics, and Synaptics Incorporated, which are also customers and partners of Immersion. We fail to see how such a high concentration of directors with ties to a single customer and partner is in the spirit of maintaining strong relationships with each of Immersion's semiconductor customers and partners.

The Board has historically been comprised of seven directors. Upon the resignation of Clent Richardson as Chief Executive Officer and in the midst of our request for Board representation, the Board unilaterally decided to reduce the number of directors by one to six. Now, the Board has decided to nominate a director with close ties to the Company's Chairman to replace Robert Van Naarden as the sixth director. It does not appear the Board is acting in good faith, and we seriously question the Board's unwillingness to add a seventh director with the attributes we believe are critical to the Company's future success.

Let us not forget that the current Board has a dismal track record of overseeing shareholder interests. As shown in the table below, Immersion shares have dramatically underperformed the market over the past three- and five-year periods. Only in the past year has the Company performed in line with the indices as it traded up from cash value following tremendous uncertainty last year during the accounting investigation that cost the Company approximately $10 million of shareholder capital.

Stock Performance (1) | IMMR | Russell 2000 | IMMR vs. Russell 2000 | Nasdaq | IMMR vs. Nasdaq | |

5-Year | (5.3%) | 30.6% | (35.9%) | 29.0% | (34.3%) | |

3-Year | (45.6%) | (9.1%) | (36.5%) | (2.1%) | (43.5%) | |

1-Year | 46.2% | 50.9% | (4.7%) | 44.9% | 1.3% | |

(1) Based on closing prices as of May 12, 2010. | ||||||

Based on the performance of the Company under the existing Board and the Board's failure to nominate a truly independent director that addresses the concerns we have outlined, we will withhold our votes at the upcoming 2010 Annual Meeting for the election of Mr. Sugishita. As we have said from the outset, we remain open-minded about solutions to address our concerns about Board composition and would be happy to discuss with you and any other members of the Board at your convenience.

We remain committed to our investment in Immersion and remind the Board of its duty to serve the best interests of all shareholders.

Best Regards, | |

Peter A. Feld | |

Ramius LLC | |

Tuesday, May 11, 2010

Equinix CIO Brian Lillie on the four attributes of a strong IT leader

Equinix CIO, Brian Lillie, appears on Forbes Video Network and gives his views on "choosing a successor" and the four attributes of a strong IT leader.

http://video.forbes.com/fvn/cio/equinix-cio-brian-lillieTech Press Reacts to Equinix Acquisition of Switch and Data

Thanks to Web Host Industry Review and David Hamilton for the mention.

You can read the full article at this link.

You can read the full article at this link.

Nokia Head of Design Marko Ahtisaari talks about priorities, competition, and future direction

from engadget:

>>Nokia Head of Design Marko Ahtisaari talks about priorities, competition, and future direction

MeeGo seems to be viewed as the platform with the greatest potential for innovation, given its larger screen, and there were some hints that those screens are only going to expand. Further probing around Nokia tablets or netbooks was unceremoniously dismissed and it really looks like the company will be knuckling down on sorting what Marko described as "truly mobile ... not luggable" hardware. One other thing he highlighted was that touchscreen interfaces nowadays require the user to constantly look at them, whereas it's in Nokia's DNA to produce devices that can be used easily with one hand or by the blind, and he left us with a big fat mystery to ponder about how that might be achieved with vast touchscreen devices. Haptic feedback (anyone heard from Haptikos lately? We're getting worried) was not ruled out, but it seemed like Nokia might try out some audio-based interface concepts and see where things might go.

>>Nokia Head of Design Marko Ahtisaari talks about priorities, competition, and future direction

Roadmap

Nokia's future roadmap is drawn around a tripartite portfolio -- you'll have S40-class f... f... featurephones (No, bad blogger! It's a smartphone!), Symbian^3 and ^4 smartphones deluxe, and MeeGo-based godzilla smartphones. We can't guarantee those particular words were used in the meeting, but the portfolio "has to be smart right across." That means a plurality of things, firstly it means that the low-end devices will not be deprived of new features, like location-aware and social networking services, but it also means "UI style innovation," which you may decode as refreshments to the grid- and list-based means by which we're used to navigating our phones today.MeeGo seems to be viewed as the platform with the greatest potential for innovation, given its larger screen, and there were some hints that those screens are only going to expand. Further probing around Nokia tablets or netbooks was unceremoniously dismissed and it really looks like the company will be knuckling down on sorting what Marko described as "truly mobile ... not luggable" hardware. One other thing he highlighted was that touchscreen interfaces nowadays require the user to constantly look at them, whereas it's in Nokia's DNA to produce devices that can be used easily with one hand or by the blind, and he left us with a big fat mystery to ponder about how that might be achieved with vast touchscreen devices. Haptic feedback (anyone heard from Haptikos lately? We're getting worried) was not ruled out, but it seemed like Nokia might try out some audio-based interface concepts and see where things might go.

PingTone Expands at Equinix's International Business Exchange (IBX) Data Center

HERNDON, Va., May 11, 2010 (BUSINESS WIRE) --

PingTone, a market leader of hosted VoIP services to government offices and businesses today announced expansion of their current data center space at Equinix's International Business Exchange(TM) (IBX(R)) data center in Ashburn, VA.

The Herndon-based company is expanding its current data center space in one of Equinix's newest and most advanced facilities. The expansion will provide space for PingTone's recently announced addition of the new BroadSoft BroadWorks plaftform as well as future planned network expansions.

PingTone chose Equinix's industry-leading data center services as it provides for best-of-breed physical security and power usage. PingTone's data center space is configured with robust cable distribution systems and dual AC and DC power distribution raceways, which can utilize Equinix's expansive diesel generators as back-up to dual power grid capabilities. The IBX data center is also equipped with security cameras and biometric hand geometry readers among other security features.

"PingTone provides a robust disaster recovery and reliable business continuity solution to its clients who view voice communication as mission critical to their business," said Glen Gaillard, vice president of Engineering for PingTone. "Equinix enables a critical component of that capability with multiple levels of redundancy and failover measures that no other data centers offer."

"This is PingTone's third expansion since we first came to Equinix in 2006. It's now the largest of our three data center facilities and we expect continued expansion in our footprint based on our rapid customer growth and expanding network requirements," said Bill Smedberg, President of PingTone. The company, founded in 1999, has 20,000 business customers for its business reliable, high quality Voice over Internet services.

About PingTone

PingTone provides Hosted (outsourced) Cisco IP phone systems to corporate, government and military customers in the United States and internationally. Organizations capture all the new operational advantages of Cisco VoIP technology without the complexity of managing these systems internally. Together with PingTone's global PSTN management, hosted VoIP service includes unified messaging, branch office 4-digit dialing and advanced call routing functions. Founded in 1999, the company is headquartered in Northern Virginia. For more information about PingTone Communications and this release, contact John Adams, VP of Sales & Marketing, 703-621-6300.

IPC extends collaboration with Equinix

from Automated trader:

>>IPC extends collaboration with Equinix

IPC Systems has announced that it has extended its affiliation with data centre services company Equinix to support demand for IPC's portfolio of Electronic Connectivity Services (ECS). Equinix already hosts IPC's core network infrastructure at three of its International Business Exchange data centres in Chicago, New York and Hong Kong. As part of the collaboration between the two organisations, IPC will extend its deployment with Equinix during 2010, adding locations in the UK and Singapore.

>>IPC extends collaboration with Equinix

IPC Systems has announced that it has extended its affiliation with data centre services company Equinix to support demand for IPC's portfolio of Electronic Connectivity Services (ECS). Equinix already hosts IPC's core network infrastructure at three of its International Business Exchange data centres in Chicago, New York and Hong Kong. As part of the collaboration between the two organisations, IPC will extend its deployment with Equinix during 2010, adding locations in the UK and Singapore.

Monday, May 10, 2010

Brigantine Advisors Reiterates a 'Buy' on Equinix (EQIX)

from StreetInsider.com:

>>Brigantine Advisors Reiterates a 'Buy' on Equinix (EQIX)

Brigantine Advisors reiterates a 'Buy' rating on Equinix (Nasdaq: EQIX), raises price target from $130 to $137.

Brigantine analyst says, "We believe the acquisition of Switch and Data will integrate rather smoothly as the combination will form a powerful and global data center offering. With SDXC’s data centers only 65% utilized, we believe EQIX will be able to offer more data center space in areas which are currently capacity constrained."

>>Brigantine Advisors Reiterates a 'Buy' on Equinix (EQIX)

Brigantine Advisors reiterates a 'Buy' rating on Equinix (Nasdaq: EQIX), raises price target from $130 to $137.

Brigantine analyst says, "We believe the acquisition of Switch and Data will integrate rather smoothly as the combination will form a powerful and global data center offering. With SDXC’s data centers only 65% utilized, we believe EQIX will be able to offer more data center space in areas which are currently capacity constrained."

Morgan Joseph Reiterates a 'Buy' on Equinix (EQIX)

from StreetInsider.com:

>>Morgan Joseph Reiterates a 'Buy' on Equinix (EQIX)

Morgan Joseph reiterates a 'Buy' rating on Equinix, Inc. (Nasdaq: EQIX), price target $125.

Morgan analyst says, "Given Switch and Data's higher proportion of Interconnection revenue (approximately 30% compared to Equinix's 12% in 2009), we believe Equinix's Interconnection business should expand as well as its network density upon integration of the two businesses. We also expect the acquisition to bring additional markets such as Miami, Denver, Seattle, and Toronto while adding to high density markets such as Dallas, New York, and Silicon Valley. Given our estimated contribution from Switch and Data, we are adjusting our 2010 and 2011 estimates. We now estimate 2010 sales and adjusted EBITDA of $1.23bn and $533mm, up from $1.07bn and $480mm, while for 2011, we now estimate $1.51bn and $665mm, up from $1.30bn and $588mm, respectively."

---

J.P. Morgan resumed coverage of Equinix with Overweight Rating and $ 130 Price Target, and Bank Of America Merril Lynch also has a Price Objective of $ 130 (Buy).

>>Morgan Joseph Reiterates a 'Buy' on Equinix (EQIX)

Morgan Joseph reiterates a 'Buy' rating on Equinix, Inc. (Nasdaq: EQIX), price target $125.

Morgan analyst says, "Given Switch and Data's higher proportion of Interconnection revenue (approximately 30% compared to Equinix's 12% in 2009), we believe Equinix's Interconnection business should expand as well as its network density upon integration of the two businesses. We also expect the acquisition to bring additional markets such as Miami, Denver, Seattle, and Toronto while adding to high density markets such as Dallas, New York, and Silicon Valley. Given our estimated contribution from Switch and Data, we are adjusting our 2010 and 2011 estimates. We now estimate 2010 sales and adjusted EBITDA of $1.23bn and $533mm, up from $1.07bn and $480mm, while for 2011, we now estimate $1.51bn and $665mm, up from $1.30bn and $588mm, respectively."

---

J.P. Morgan resumed coverage of Equinix with Overweight Rating and $ 130 Price Target, and Bank Of America Merril Lynch also has a Price Objective of $ 130 (Buy).

Sunday, May 9, 2010

Immersion 1Q results: unexpected upside

Immersion (IMMR) reported 1Q 2010 results on May 6 (see Company’s P/R and Seeking Alpha transcripts).

Let's go through some of the highlights:

- Revenues were $9.7 million, an increase of 29% compared to revenues of $7.5 million for the 1Q of 2009 and an increase of 41% compared to $6.9 million in the 4Q 2009;

- Net loss for the first quarter, was $(2.7) million, or $(0.09) per share - however, this result was impacted by about $1,6 million of costs related to the recent investigation/restatement;

- The Company ended the quarter with $ 64,6 million of cash and cash equivalents, a slight increase on the $ 63,7 million available at year's end (as a reminder, Immersion has no debt)

- Immersion completed the build-out of its senior management team with the appointment of a new CFO, Shum Mukherjee

- The annual target of revenues of $25 million to $30 million was reaffirmed, with revenues in the 2Q to be expected in the range of $6.2 million to $6.7 million (more on this later on)

As some of you may remember, Immersion had given guidance for the 1Q during its last conference call:

While we don’t expect to provide quarterly guidance regularly, given that we are at March 30, it seems prudent to give you a little color on expected Q1 results. We anticipate total revenues of approximately $8 million with royalty and license revenues comprising approximately $6 million.

Given the fact that guidance was given so much into the 1Q, the actual numbers came as a surprise. During the Q&A session, this was the subject of a specific question by Mark Argento (emphasis added):

Mark Argento – Craig-Hallum

And I apologize should I hopped on the call a little late, but you guys reported almost close to 10 million, what was the delta given the fact that you guys gave guidance late in the quarter that ended up driving that an extra almost $2 million in upside of the revenues?

Victor Viegas

I think we said we were somewhere in the $7 million to $8 million range was our guidance. And at the time that was about estimates that I had, we ended up the quarter at $9.7 million as you stated. When we announced that we’re transitioning out of the medical product line business there was some concern that the orders for that that market area would dry up or change significantly. At the time we didn’t have all the royalty reports in hand, we hadn’t yet done full analysis of all the contract revenue, and there’s always late in the quarter, contractual commitments, whether it’s delivering a product, or achieving a milestone, and those are sometimes that risk.

And so, again, when I gave the guidance it was my best estimate at the time it turns out this quarter, there’re obviously quite a few things that occurred late such as the product fitments for our medical and deliverables and contract signing. So, very happy to be pleased to report on a positive in the upside of that estimate.

Mark Argento – Craig-Hallum

I just want to make sure was it like a one-time event that came in or it was just the business outperformance; it sounds like that’s the case.

Victor Viegas

It was not any one-time event, it was solid results across the board, and again, if revenue comes in from royalty reports, contracts, service agreements, NRE agreements and product shipments, and so I think you’ll see a lot of hard work from a lot of people resulted in a good quarter, but not a one-time event.

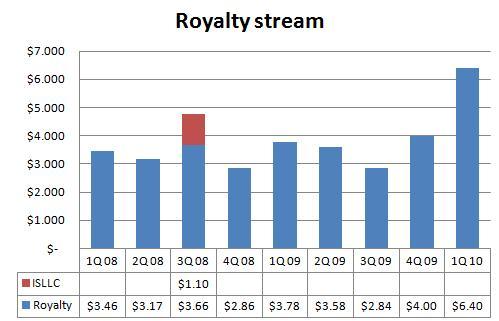

If we have a look at the historical numbers, this looks definitely like a break out quarter (click to enlarge):

As we know, Immersion is transitioning toward a licensing model only, so it may be appropriate to focus on royalties and license revenues only:

If we go through the 10Q, we learn that this result was due to an increase in sales in most segments (pg.31):

Royalty and license revenues increased by $2.5 million mainly due to increases in royalty and license revenue from mobility, gaming, touchscreen, integrated circuit, and automotive licensees. We expect royalty revenue to be a significant component of our revenue as our technology continues to be included in more products along all lines of our Touch business.

The effect of seasonality in these numbers must not be forgotten (the year end holiday period has a positive effect on sales of a few verticals like gaming and mobile phones, whose royalties are recognized in the 1Q), still we see it as a positive that even internal Company's expectations were beaten when the actual sales results came in.

A few words about the medical segment. As we know, Immersion sold the Endoscopy, Endovascular, and Laparoscopy medical simulation product line to CAE Healthcare on March 30. The selling price is about $ 1,6 million, and the agreement also provides for the transfer of approximately 35 employees to CAE as well as distribution agreements and customer relationships.

As a result of this shift to a license and royalty model, Immersion is expected to reduce expenses of about $ 1 million a quarter:

Aaron Husock – Lanexa Global Management

Okay. So was the medical related OpEx only a $l million in the quarter, it’s roughly a third of the workforce, right?

Victor Viegas

You’ve got some of the people are in the cost of goods sold, so, it’s a different mix and I don’t have a precise set of numbers, we don’t’ really disclose that that closely. So it’s in that $1 million range is what I’m using to arrive at $8 million in total touch expenses.

Another side effect of the sale of the medical segment to CAE is that Immersion will not be receiving royalties in the 2Q related to this segment (10Q, pg. 15):

The Company will receive quarterly payments under the license arrangement starting July 1, 2010.

While this may sound logical (CAE royalties, like for all other licensees, will be recognized in the subsequent quarter), it will effect, short term, Immersion's results in the 2Q, as the Company will receive no royalties but will lose a business segment that contributed about $ 2 million in sales in the 1Q 2010. This might, together with seasonality, partially explain the guidance issued by the Company.

Aaron Husock – Lanexa Global Management

Okay. Looking at the guidance, would you say that $7.7 million is kind of the right number for us to compare your guidance to, $7.7 million in revenue in Q1, is that kind of the steady state number that we should be comparing the $6.2 million to $6.7 million?

Victor Viegas

Yes, I think that’s the right comparison. I think the $7.7 million you arrive at that as a $9.7 million minus the products revenue from the products that we transition to CAE. So I think $7.7 million compared to $6.2 million to $6.7 million for Q2 that's an apples-to-apples comparison.

During the conference call, a new licensee was revealed:

Also during the quarter Alcatel-Lucent (ALU) became a new licensee in the office product sector and they recently showed of their OmniTouch 8082 IP phone featuring Immersion haptic technology. The user interface features a 7-inch wide capacity of Touchscreen that is LED backlit and includes context-aware, sensory feedback with Immersion’s TouchSense technology.

The product is very interesting, and opens a new market to Immersion - here is how Alcatel-Lucent describes this new category of Smart Phones:

ORLANDO, March 23, 2010 – Alcatel-Lucent announced today an innovative new class of “Smart DeskPhones” that transforms a desk phone into a rich communication experience beyond what mobile smartphones provide. The new phone brings together enterprise reliability, fast, convenient access to multimedia communications capabilities and web applications to create personalized mashups or industry-tailored applications.

The Alcatel-Lucent OmniTouch™ 8082 My IC Phone ushers in a new era of software access and sophistication never before seen in a desktop phone, and redefines what users can do from their desk. Unlike traditional desk phones, the new device offers an open platform and an entirely new user interface based on a large multi-touch display. Powered by pioneering new software and an open interface, it has a seven-inch wide capacitive touch screen that is LED backlit and includes context aware sensory feedback, as well as connectivity to Bluetooth and USB devices.

It must be noted that the product will start shipping in late 2010 – a remaining issue with Immersion is the long selling cycle from product development to the time royalties are recognized, as also described for the semiconductor partners in this section of the Q&A:

Aaron Husock – Lanexa Global Management

Okay. Just one more, if you look at your partnerships with the different semiconductor vendors, Atmel, Cypress, IDT, and now Renesas , was there any revenue from those partnerships in the March quarter and if not when do you think you will start to see some level of revenue there?

Victor Viegas

I don’t know if I have a number for you or if there was any revenue in the quarter I can tell you Renesas has been shipping chips, they have a product in the market and there’re consumer products. I know there is a P&D [ph] product in the market, so we’ve been generating revenue from Renesas here for a bit. In terms of Cypress and Atmel, I think those two products are expected to come later this year.

Even the newly announced “HD haptics” solutions, which should bring higher per unit royalties, will mainly have an effect on revenues later in the year:

Our latest haptic solutions are being very well received by our current and prospective OEMs, with TouchSense 4000 currently available and shipping in our partners’ products. And TouchSense 5000 expected to ship in commercial mobile handsets in the second half of this year.

As the Company isn't exactly on many investors' radar screen, Immersion will also be soon presenting at several conferences, like the JMP Securities 9th Annual Research Conference, the MDB Bright Lights IP Conference and the TechAmerica Growth Cap Financial Conference.

As a last side note, a new candidate for the BoD has been nominated:

the Company’s candidate for the Board seat to be vacated by Rob is Dave Sugishita. David currently serves as Chairman of the Board of Atmel, where he chairs the Audit and Corporate Governance and Nominating Committee and is a Director and Chairman of the Audit Committee for Ditech Networks.

It is not clear if Ramius was involved in this decision – as a reminder this fund took a large position a few months ago, and has recently been selling a few shares, slightly reducing its position in the Company.

Subscribe to:

Posts (Atom)

{kind=link}